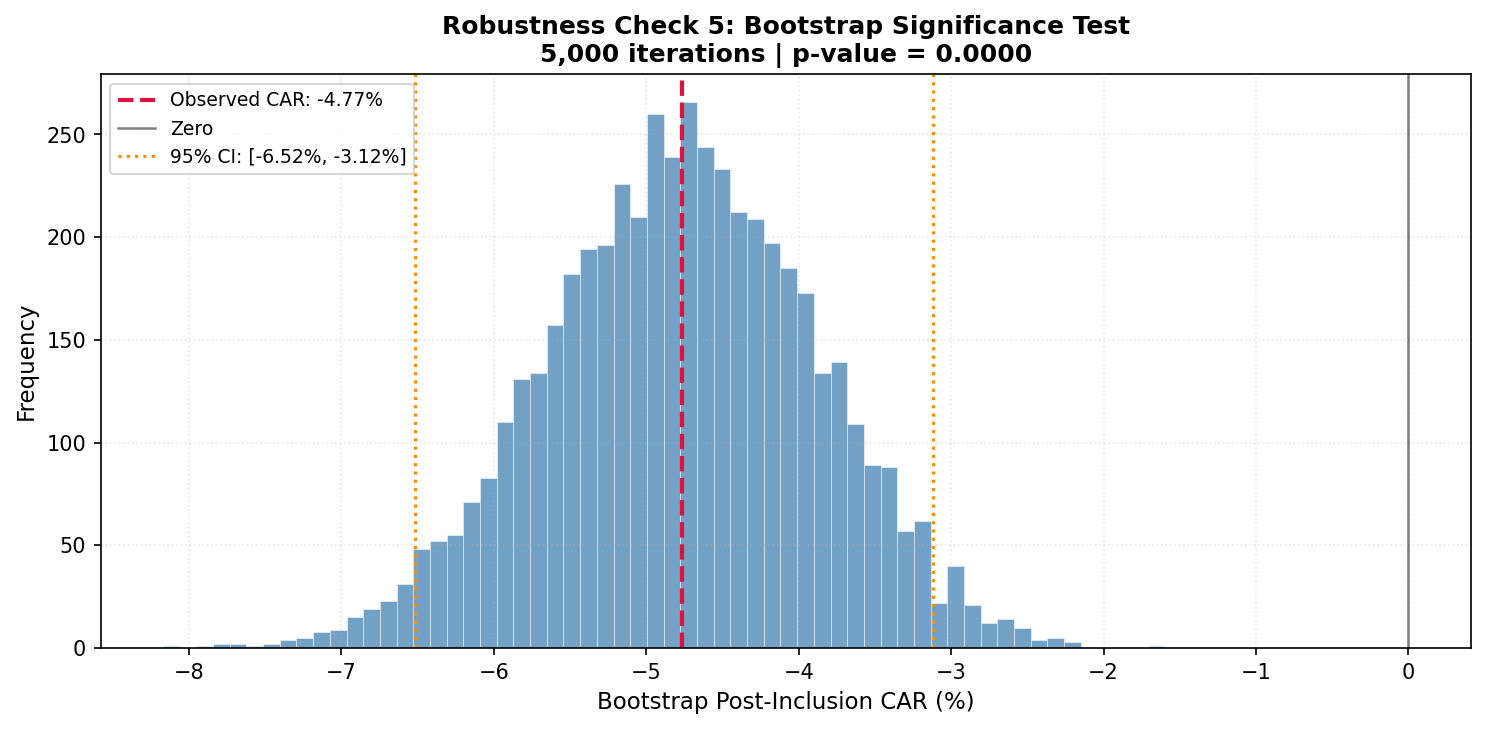

Trading Volume Around Inclusion

A massive volume spike of +1,813% on the day before effective inclusion reveals intense index fund front-running activity. Elevated volume persists for 20+ days as passive funds complete their rebalancing.

Average Abnormal Trading Volume (AAV)

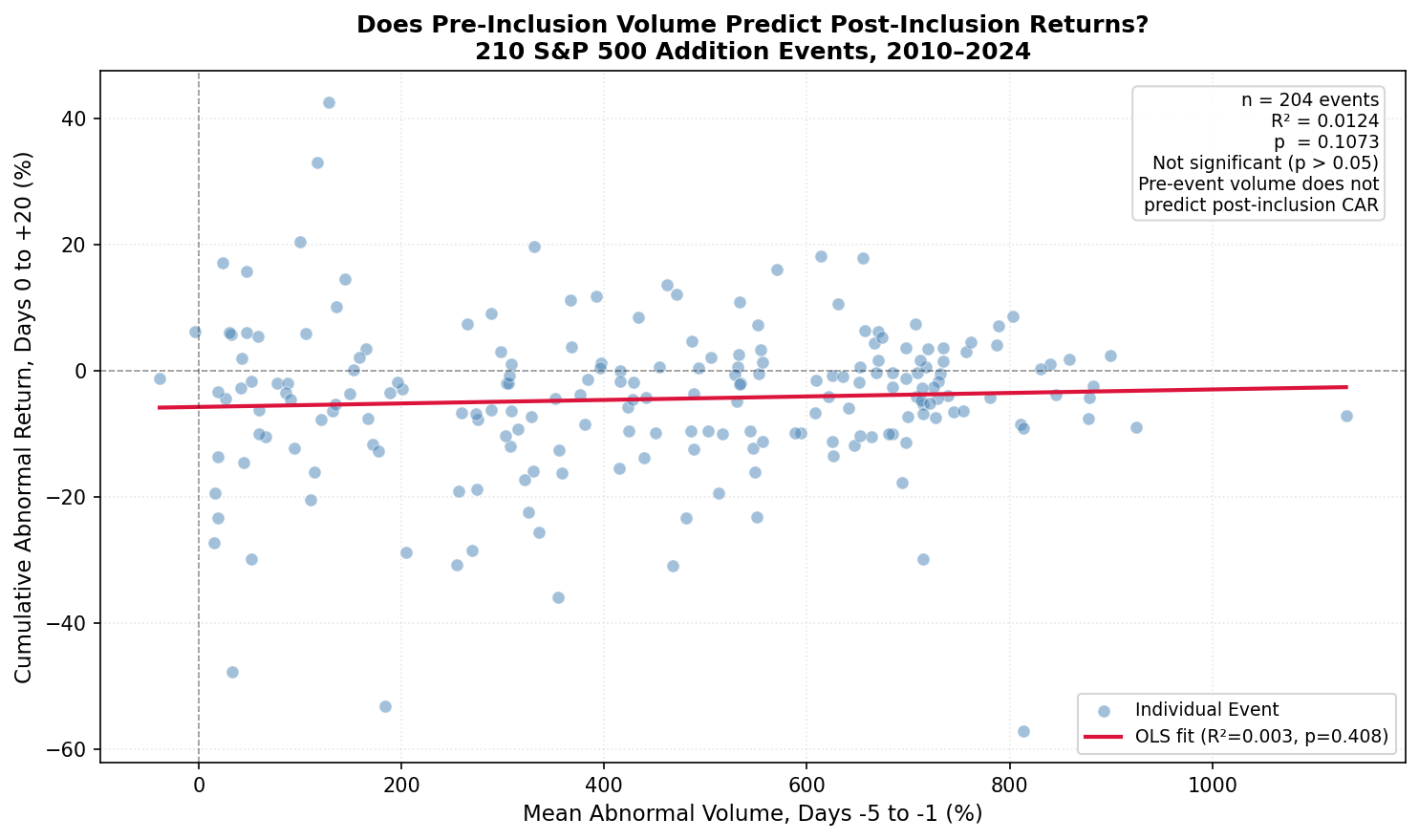

Does Volume Predict Returns?

Pre-event abnormal volume (days −5 to −1) vs post-inclusion CAR (days 0 to +20) · N = 210 events

Volume Mechanism Identified

The day −1 spike is driven by anticipatory trading ahead of the known effective inclusion date. Index funds must buy the newly-added stock; their predictable demand is front-run by active traders. The buildup begins as early as day −5 (+58% abnormal volume) and accelerates sharply into day −1.

Volume Does NOT Predict Return Magnitude

Despite the dramatic volume spike, pre-event volume levels have no statistically significant relationship with post-inclusion underperformance (R² = 1.24%, p = 0.107). Volume is a symptom of the structural demand change, not a signal of how large the price correction will be.

Persistence of Elevated Volume

34 of 41 event-window days show statistically significant abnormal volume. Post-inclusion, volume remains elevated through day +20 as index funds continue accumulating the new addition — a multi-week process reflecting the scale of passive fund rebalancing.